|

From a planning perspective, we have found that one of the areas that tends to cause the most amount of confusion, and misinformation, is Social Security claiming strategies. Unfortunately, many of the resources available to those approaching social security age seem to only compound the problem. Employees at your local Social Security Office can be a good resource, however, it is important to keep in mind that their job is to provide you with information: They are not advisors and will not tell you what to do.

How Do I Maximize My Social Security Benefits?

The rule of thumb is that delaying taking benefits is the best approach, however, you do take on the risk of needing to live long enough to make up for the years you have deferred collecting benefits. Your benefit grows 8% each year you wait to begin collecting benefits after Full Retirement Age. If you choose to defer benefits it is important to understand where your break even point is.

Even if you choose to delay benefits, there can be some interesting strategies (especially for married couples) to begin collecting some benefit at full retirement age and still allow your lifetime benefit to grow. If you think you need the income prior to age 70, the delay method still works well if you have other assets that are conservatively invested which you can draw down while allowing social security to grow. Many of the creative claiming strategies for married couples become possible once both spouses have reached “Full Retirement Age”, currently 66.

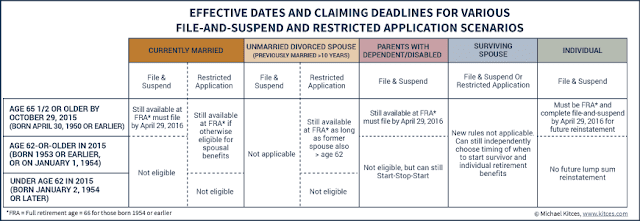

File & Suspend/Filing a Restricted Application

We wanted to highlight one strategy that couples can use to maximize benefits. This is just one example of the many strategies you can implement. The right strategy for you will depend upon a number of factors including age, your health, your need for income, your other assets, how much you’ve paid into the system, etc.

In the example below the goal is to maximize benefits for both spouses, who believe they have a long life expectancy. The key to this claiming strategy is that both spouses are at Full Retirement Age when they make the initial claim. In this example one spouse is 66, and one is 68.

![]() |

By choosing this strategy over simply both deferring to age 70

they are able to collect an additional $57,600 over the four year period. |

Our View

The difference in claiming strategies for social security could add up to hundreds of thousands of dollars over your lifetime. Given that, we feel it should be an important enough part of your overall portfolio and income plan to spend some time analyzing what solution will be right for you.

If you have a financial advisor they should be helping you with this planning. There are also some fantastic resources out there for Do It Yourselfers. www.socialsecuirtysolutions.com, www.maximizemysocialsecurity.com & www.aarp.org/socialsecuritybenefits all offer free or low cost calculators that will help you compare claiming strategies. Just make sure you understand what the calculator is solving for (maximizing monthly benefits vs. maximizing lifetime benefits) and that the solution it recommends fits with your overall plan. At the very least, you should establish free online access to Social Security (www.ssa.gov) where you can see the estimates they provide and use the online calculator.

We don’t know what SSI will look like for those in their 30s, 40s and even 50s. There is a lot of discussion about what the social security system will look like in the future (or if it will exist at all), that is not for this discussion. We feel it is safe to say that for those 55 and older it will be a part of their overall lifetime assets, and is therefore worth some time to make sure you are maximizing it.

|