Last month, Professor Rene provided an update of the current market given the recent downturn (see below). Given the continued volatility here is an update to that update.

With yesterday’s announcement of reciprocal tariffs the market is now down -13% from its Feb 19 high. Since my last post of Friday March 14 the market was actually flat through yesterday. But today the news hit the market hard and we saw a -5% drop for the day.

We know there is a ton of anxiety out there. In emotional moments like this it is my job to be cold and clinical in evaluating the short-term and medium-term implications.

So a few things to reflect on:

- In ‘18 the market dropped -20% in reaction to the first wave of China Tariffs. From early October to Xmas the market was in free fall. But by May of ’19 it had fully recovered.

- This round of tariffs is much wider in scope, but it has also been well telegraphed, so the market has known the direction of travel, if not the full magnitude.

- In the short run there could be further declines if our European and Asian counterparts take steps to restrict purchases of American goods or to tax (or even boycott) American Social Media firms like Google/YouTube, Meta/Facebook, etc…

- A protracted trade ‘divorce’ could tip us into a recession… but it is not a foregone conclusion. Economically, our trading partners have much more to lose by retaliating.

- If we do slide into a recession the Fed has plenty of room to cut interest rates and to soften the blow. Our banking system is very well capitalized and should continue to lend even during a recession. (this is NOT a Lehman Brothers type of ‘storm’)

- Looking out beyond the next 12 months, I do not believe that higher import tariffs will meaningfully harm the long-term ability of Corporate America to drive profit growth (which is the lifeblood of our markets).

- There will be a period of adjustment in the short term but U.S. companies are adaptable and there will be stimulus coming in the form of tax cuts and deregulation.

- Finally, we should not rule out the possibility that more European/Asian manufacturers move production to America or that more export markets open up to American companies, as a result of these negotiations.

As this saga plays out in the coming weeks, we are of course advising clients to stay the course.

In the meantime, we remind you of our investment philosophy:

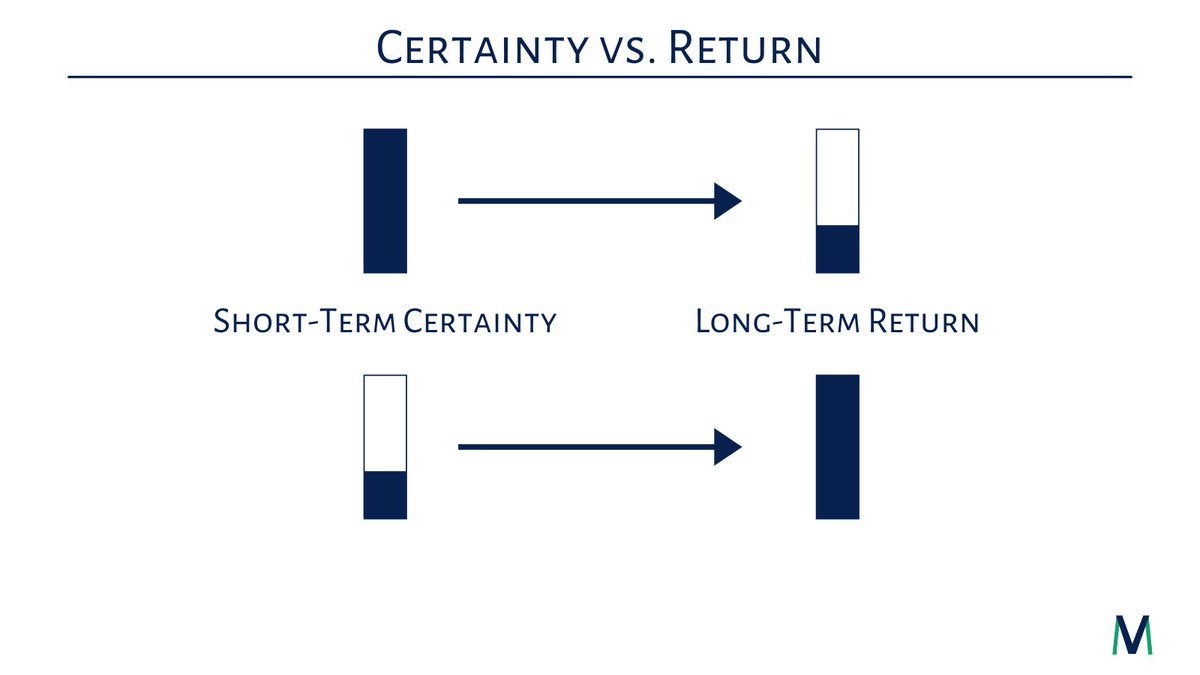

…at Single Point the main risk we seek to mitigate is the risk of permanent loss of capital, which happens only if we liquidate positions during the ‘storm’, versus waiting until the storm has passed. We construct portfolios with the full expectation that market declines – both shallow ones and deeper ones – are a fact of life, albeit with different frequencies.

From March 14, 2025

For now, the S&P 500 is down 8% from its recent (all-time) high on Feb 19.

It’s an uncomfortable feeling not knowing whether an 8% drop will turn into a 25% bear market, but some things in life are unknowable – even to the most astute investors.

It is key to remember that through all the previous market downturns, it has always recovered. Usually quickly (Post-Covid in ‘20) but sometimes slowly (Post-Lehman in ’08-‘13); but it’s during these abrupt declines when our emotions threaten to overrule our more rational instincts.

As you know, at Single Point the main risk we seek to mitigate is the risk of permanent loss of capital, which happens only if we liquidate positions during the ‘storm’, versus waiting until the storm has passed. We construct portfolios with the full expectation that market declines – both shallow ones and deeper ones – are a fact of life, albeit with different frequencies.

Knowing that the markets have always recovered, the key is to make sure our clients have sufficient cash and bond buffers to ride out the bear leg of the cycle for an extended period of time. We model those bond buffers on the assumption that the recovery of stocks could take several years – in a stress test scenario. These buffers allows us to raise cash without being forced sellers of stock, as well as to buy additional equity exposure at ‘a discount’ with proceeds from bond/cash. This framework has underpinned our approach to portfolio construction, and has served our clients well through many corrections and bear markets.

According to research by Jurrien Timmer of Fidelity, since 1927, ‘mild’ corrections of -5% have happened 57% of the time, while drops of -10% have happened 37% of the time. Bear markets (-20% or greater) have happened 20% of the time, yet over the long-term, the stock market has compounded at 11% per year. (see graph below)

The political backdrop notwithstanding, investing is ultimately about math and these are good historical stats to keep in mind while we worry about what comes next.